The Long Blog! This pairs with our podcast special... Past, Present, Future.

The Bubble(s) is Here?

When investing, it is critically important to understand how markets arrive at their current position in order to divine the potential future. To do this we use a mix of our 8 investment principles, long term historical valuations, and shorter term events from the current cycle. At this late stage of the bull market, you will hear the well worn saying "this time is different". We aim to show “this time is different” is a dangerous statement.

In this 3 part series, we want to explain how we got here, Using the current mania surrounding the potential of the artificial intelligence sector, we will show similarities of the current cycle and why it is no different from all the previous cycles where the stock market has periods of outperformance followed by periods of underperformance. However, there are asset classes we believe will outperform over the next decade and we will lay out our arguments here and on our other platforms.

The Beginning of the Bull (the past 16 years)

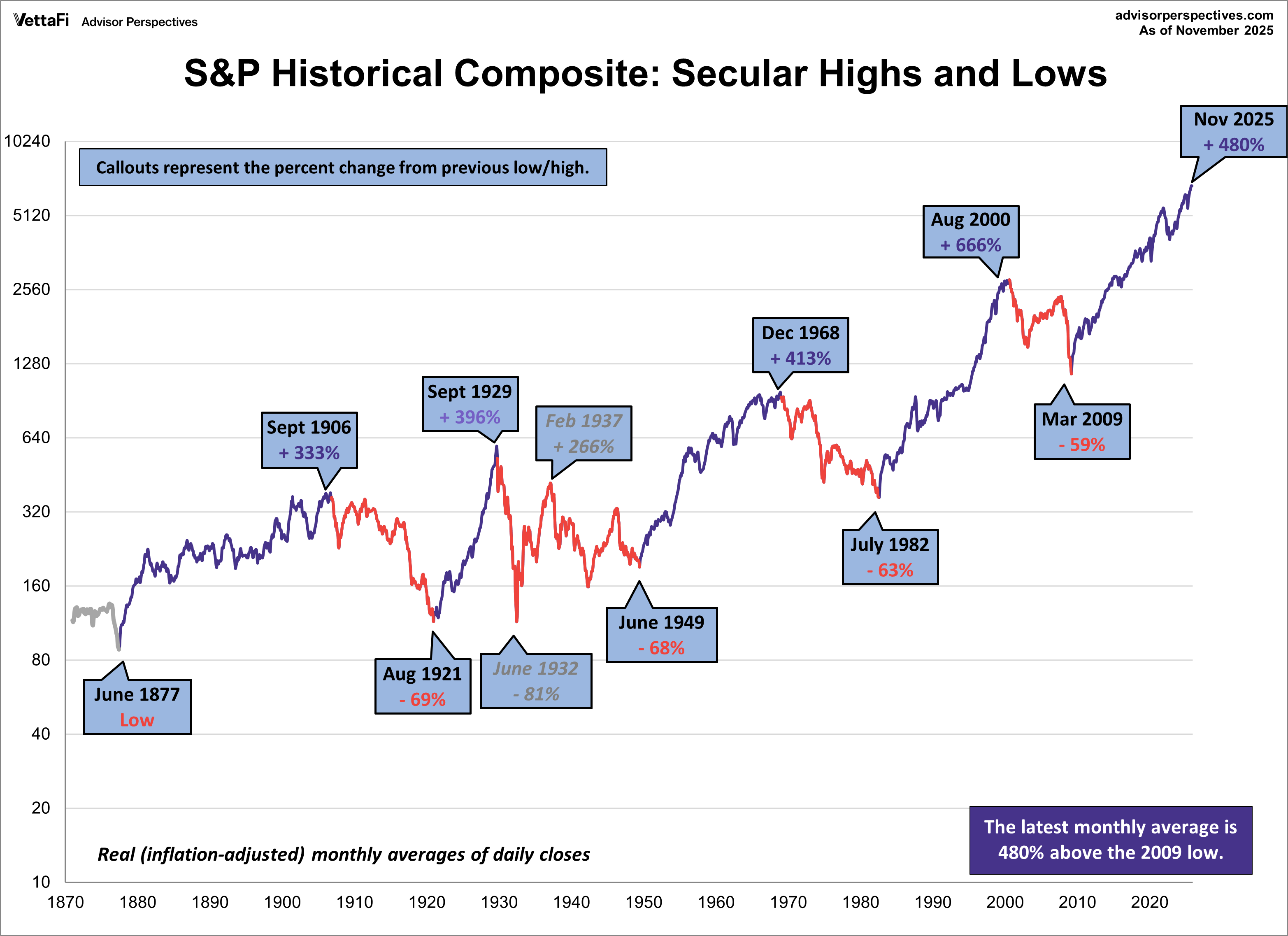

This bull market cycle started in with the low on March 9, 2009 and has seen spectacular returns for those who have held through thick and thin. But placed in an historical context, we should perhaps not be surprised when you see that it is largely a standard bull market commencing with a low valuation. This time is not different.

In The Beginning

I call tell you that in the decline of 2008/09, the stock market was the last place anyone wanted to be invested. The GFC was sufficiently traumatic to put many investors off investing for an extended period of time. The world’s governments, led by the US were required to save capitalism. As Bush said “this sucker is going down”.

In 2009, the CAPE was 14. A time to actually invest heavily. Warren Buffett's advice “Buy American, I am” was to pay off handsomely over the next 16 years.

As usual Buffett was correct, but like many contrarians, shouting into the void, most investors either counted their losses from the GFC or were too inexperienced and gun shy to enter a highly volatile market. It does take some fortitude to enter a market after a life changing event especially when it is a large loss that impacted the lives of many.

Following 2009, Europe too experience economic trauma when Greece fessed up that things were not as rosy as they had been making out (in Buffett’s term they were swimming naked and the tide went out) and required the rest of Europe to bail them out. Greece wasn’t alone as Spain, Ireland and others all realised how interconnected their economies were and reliant on the US consumption for a majority of their performance. Greece escaped jail in 2018, but not before some serious issues were raised about how Europe planned to hold together. Since then Europe has lagged the US by a long way.

Emerging markets too had issues as the China boom rolled on, but in 2011 rolled off. And hard. Commodities delivered large profits to most Australians, but when supply rose meeting demand, prices fell. Our stock market after reaching a CAPE high of 31 in 2007 has underperformed the US in part because we had to work off the excessive valuation.

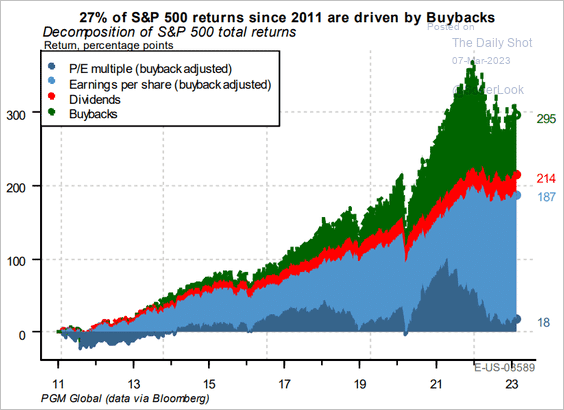

Share Buybacks

Thanks to cheap money from low interest rates and large government deficits, companies took advantage to re-purchase their stocks. These buybacks drive earnings per share higher since there is fewer shares for profit distribution. The chart below shows that company buybacks have been a significant driver of market returns. Without these buybacks the US market would be 30 percent lower than it currently is.

The chart shows the impact stock buybacks have had on the market over the last decade. The decomposition of returns for the S&P 500 breaks down as follows:

- 6.1% from multiple expansions (21% at Peak),

- 57.3% from earnings (31.4% at Peak),

- 9.1% from dividends (7.1% at Peak), and

- 27% from share buybacks (40.5% at Peak)

The US as is usual recovered and boomed again as investors returned to drive solid returns during the 2010’s.

Every cycle has its stars and this cycle is no exception. With the usual doubts and fears the market climbed and as it has matured, there have been numerous displays of irrational exuberance with much of it around technology and its promises of a brighter future.

Below is a list some example of bubbles. Note that most, f not all of these are sold as "game changing" innvations that eventually fade into obscurity with most investors losing money.

- Rare earths

- NFTs

- Meme Stocks

- Cryptocurrencies

- AI

- Metaverse

- Robotics

- EVs/FSD

- Medical marijuana

- Shale oil

- Private equity

- SPACs

- Covid stocks - Zoom, Peloton etc.

- ZDTE Options

- Leveraged ETFs

- Real Estate

- Robinhood trading platform

- NASDAQ 24 hour trading

Famous Faces - From Heroes To Zeroes

In all cycles, there is an increase in scams and illegal behaviour as cheap money floods markets and gullible investors are lured into large returns that don’t last.

Each cycle has its stars mainly those young enough to be presented as the face of the future. They are cutting edge, ruthless, focussed, discipled and relentless. They are also rule breakers to the point that some are actually criminals. But they are held up as representatives of this ‘new era’ and to be emulated.

Sam Blackman Fried - crypto king. Bankman-Fried founded the FTX cryptocurrency exchange and started showing up in all the usual places surrounded by celebrities. He and his partner were convicted of fraud and related crimes in November 2023. SBF is now in jail.

Elizabeth Holmes - was a CEO and hailed as the new Steve Jobs. Holmes founded Theranos - a now-defunct health technology company that falsely claimed to have revolutionized blood testing with a device that could perform a wide range of tests using only a few drops of blood. The company was valued in billions before its claims were exposed as fraudulent. The scandal led to legal action against Holmes and other executives, and the company ultimately ceased operations. Holmes is now in jail.

Michael Saylor - Microstrategy - FUN FACT: In 2000, Michael Saylor lost over $6.8 billion in a single day, making him the biggest loser of the entire dot-com bubble. His company, MicroStrategy, was also charged by the SEC for fraudulently cooking the books and deceptively reporting a profit despite operating at major losses. The firm should have gone bankrupt, but Saylor quietly cut a deal with regulators, paid a record settlement under confidentiality, and secured a bailout from a consortium of foreign investors. As the saying goes, history doesn’t repeat, but it often rhymes. Saylor was once a vocal Bitcoin critic, even comparing it to poker and gambling. He is now flogging a deeply flawed Bitcoin strategy to the public. MSTR is down 50% in 2025 and 65% from the all time high.

Elon Musk - where do you start? Musk’s grift is so long, there are simply too many to consider in detail. However, the self-proclaimed free market capitalist is one of the greatest beneficiaries of government spending. Since 2003, Musk and his businesses have received at least $38 billion in government contracts, loans, subsidies, and tax credits.

Travis Kalanick - Uber founder who consistently broke the law was eventually ousted by the Board for a myriad of issues including abusing an Uber driver and not dealing with Uber’s sexual harassment issues within the company. But he made billions.

Adam Neumann - Neumann was famous for being barefooted and smoking a ton of pot. He was the epitome of cool. WeWork, once a high-flying startup valued at $47 billion, experienced a dramatic downfall, culminating in a Chapter 11 bankruptcy filing in November 2023. The company's struggles stemmed from a combination of factors, including questionable governance practices under CEO Adam Neumann, an unsustainable business model, and a failed initial public offering (IPO).

Chamath Palahapitiya - Chamath is back in August 2025 with a new Special Purpose Acquisition Company (SPAC) - American Exceptionalism Acquisition Corp (AEXA) which will raise $250M by selling 25M shares at $10 each. The high profile face of the SPAC industry has not really made it based on past performance of his prior SPACs. Since their debut: Opendoor (-65%), Clover Health (-74%), and Virgin Galactic (-99%). Also a billionaire.

Peloton - or known as an iPad on a bike. Hit the big time during Covid when gym junkies couldn’t get their fix due to lockdowns. The bikes and programs varied but it was not uncommon to see them prices at $3,000. Peloton had supply chain issues with months long delays for bikes that irked new customers. Then, a disastrous recall affected both of its treadmills: the Tread Plus, because it injured several users and killed a small child, and the regular Tread, which hadn't even launched because of a wobbly screen. Peaked at $162, now at $7.74

Beyond Meat (BYND) - Saving the planet seemed like a profit making opportuniy regardless of the science which showed vegan diets (another fad) are lacking in many basic nutrients. Needless to say, their initial hype could not be sustained as people worked out that mixing a bunch of chemicals to make it taste like meat, doesn’t actually mean it is meat. BYND launched at $66 in May 2019 peaked at $235 US dollars in July 2019. It is currently $0.82 (not a typo).

This market cycle is no different from any of the previous market cycles and they repeat with similar characters and patterns of behavior.

We will now discuss the present market using the AI sector as a representative of how markets have taken on an aura of invincibility.

This time is not different.

The Present

When valuation runs well ahead of fundamentals and investors are struck with FOMO, markets that have gotten well ahead of themselves invariably at some point deliver a reality check for investors.

That is not reason for pessimism. While the tech sectors spectacular returns have led to an expensive market, there are undervalued sectors and countries for those who are prepared to maintain disciple and take a long term view. That's why we believe there are a number of opportunities ahead and we will detail these in future editions. Hopefully we can convince you that markets do cycle and we can assist you to take advantage of the cycle’s ebbs and flows.

We are by no means calling a market top. We are not foolish enough to believe we can predict what is going to happen over the short term, or approximately six months. We know from studies it is impossible to determine which straw breaks the camel’s back or which grain of sand collapses the pile.

We don't need to know which individual grain collapses the pile but given the size and growth of the pile you can see it is becoming increasingly susceptible to an event which becomes the catalyst for the inevitable collapse. So, a now 16 year bull market with the CAPE ratio rising from a low of 12 to a high of 40, we know the longer this goes the more pain and losses there will be.

One of the valuable aspects of determining the market fragility is directing the gaze of an investor to potential losses rather than expected gains. It also gives an investor the opportunity to think about the consequences of left tail events which may have a low probability but very large consequences. However, every time without fail where CAPE has reached these levels it has resulted in crashes of some magnitude. This time isn't different.

The difficulty is in determining exactly where we are in the market cycle - are we at the start, the middle or closer to the bursting? Below is an 8 minute video which succinctly describes the issues.

|

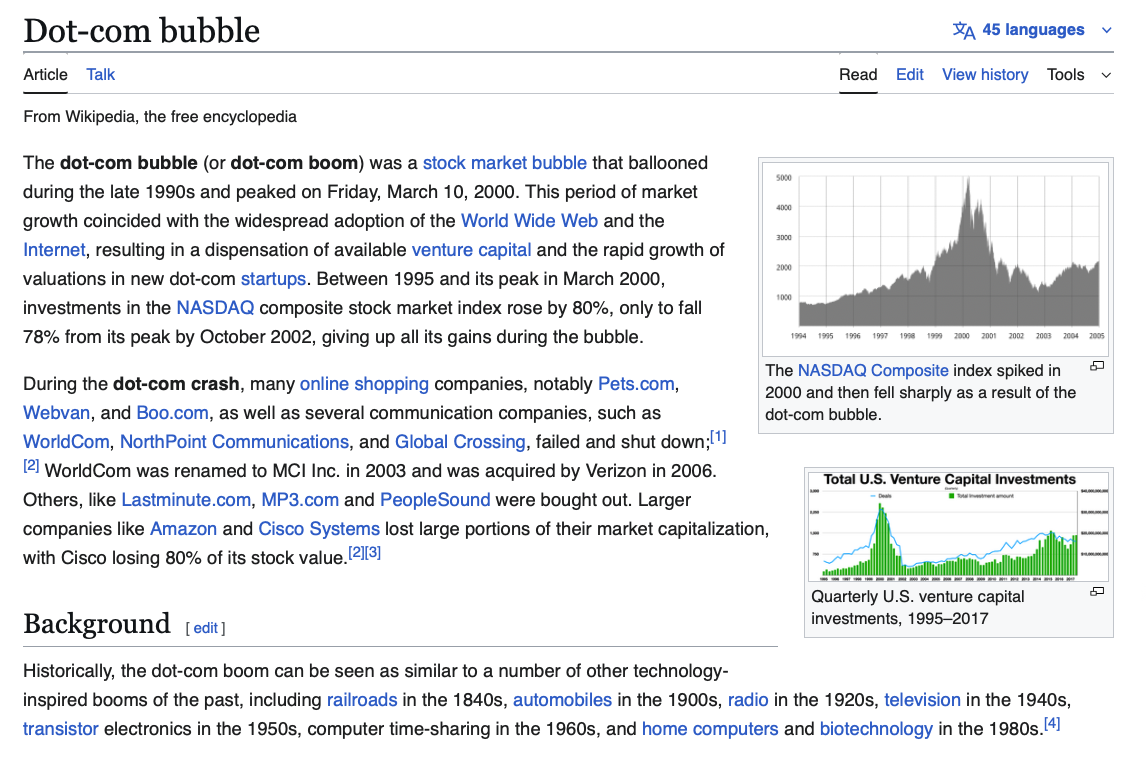

In this section we discuss what we see as the greatest threat to bursting the bubble. That is the artificial intelligence (AI) sector. It is fair to say it has exploded over the past 5 years since covid and is now completely overwhelming all other sectors and accounts for an overweight proportion of US indexes. Needless to day we think AI is now a systemic risk to broader markets much the way the dotcom bubble saw the NASDAQ lose 82 percent and the S&P around 50 percent from 2000-2003.

We need to make clear here we are not predicting the fall of the AI industry to a point where it will turn out to be a fraud or complete failure. What we are saying however, is to deliver the returns investors expect, you need to suspend rational judgement and consider just how the industry would need to perform to achieve investors expectations and company valuations.

We don't believe these companies will be able to deliver on the promises or the shareholder returns that most anticipate. We think of it like the railway and the telecom/internet boom. While both succeeded in changing the economy and society, on both occasions investors paid a heavy price in terms of investment losses.

Here is a brief description of the dot com bubble.

You know you have to listen when insiders like Altman are saying AI is a bubble.

We don't want to get bogged down in the weeds, so we will just highlight some analysis and numbers. But remember just because the market price of these companies is rising, it doesn't mean they are valued rationally.

AI data centers are hot property at the moment since they are required in large numbers for the AI industry. Energy and water are also huge inputs into making AI successful.

Data centers are taking in huge amount of money (capital expenditure or cap-ex for short). That is not necessarily a bad thing but that investment needs to make a return. So far, no one can make it work economically.

AI is using the latest cutting edge chips, but these chip costs which are huge, need to be expensed (through depreciation) over 3 years. Basically you spend $100 on chips, then expense it at say $33 a year, but in 3 years time you need to spend more funds to buy more newer chips.

Cap-ex spend by the Mag 7 is around $560 since 2019 with revenue of aprroximately $20-$30 billion. Depreciation estimates coming in at around $40 billion annually meaning revenue does not cover expected depreciation.

This leads to negative cashflow (but the promise is more revenue comes when more customers sign up and pay once they see the benefits). To make economic sense revenues would need to be somewhere around $480B revenue in 2025, far above current run rates.

The revenue increases needed are unlikely to be reached in the expected timeframe before depreciation costs and other expenses. User numbers may well slow given the well publicised problems with AI to deliver on the promises. This is exactly what happened in the dotcom bubble with laying internet cable - huge capital spend based on future promises that failed to arrive. On top of this, job displacement and productivity benefits may also be overstated.

|

We know AI valuations are rich, and we don't want to go through every single potential problem with a microscope, but simply highlight some major issues which look to be rhyming with the dotcom bubble.

It is important for investors at this stage of the cycle to cast a skeptical eye over most of the promises that industry leaders are announcing as there is already considerable reversal of some previous promises.

That does not bode well for the near future.

The Future

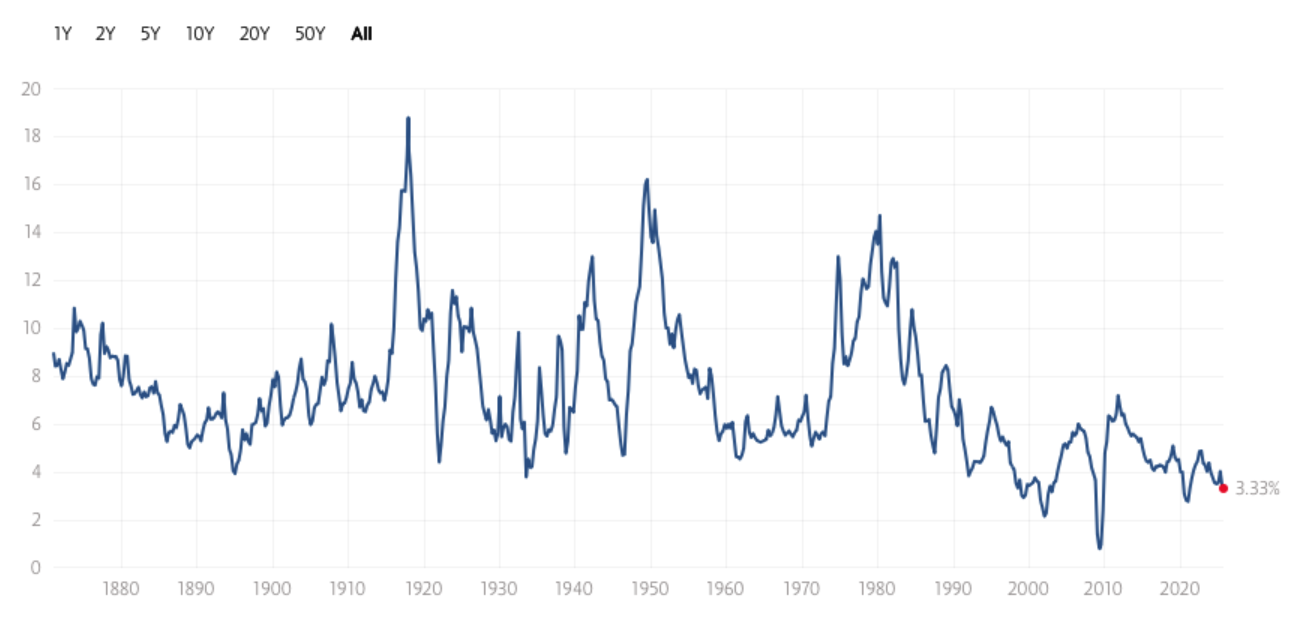

Because valuation has a strong correlation with future returns, we should be able to understand the future by looking at the past. Along with other valuation metrics, we expect US markets to underperform over the next decade because the CAPE has moved from a low of 12 to a now high of 40 . Any serious analysis would be hard pressed to justify average returns over the next decade considering the overwhelming evidence to the contrary. If the CAPE was to revert from 40 to 15, then we would change our mind.

The histogram below shows that expensive markets deliver below average returns. Focus on the 10 year and 20 year rolling returns and you will see confirmation that high valuations see lower future returns. The returns do not include, fees, taxes or inflation.

Below is the historical earnings yield showing low future returns from high valuations.

However, falls from all time highs to lows can often take years and go through shorter term cycles which is why we introduced some simple technical analysis to our systematic approach.

We believe this US bear market will be secular (long term) not cyclical (short term) meaning we may have a zero return over the next decade and maybe more. We are not being sensationalist here, but simply putting together a scenario based on historical returns and current shifts taking place in the global economy.

US INVESTMENT BOOM

It’s not just valuations that reveal future returns.

After 40 years of globalisation, the US has changed tack and is now in the process of asset (re)building as it revives its domestic manufacturing industry. The days of cheap goods and services made in low wage countries like China is over.

The US gave up its manufacturing industries starting in the 1980s and has experienced a severe hollowing out of most of its manufacturing sector, first by Japan and Europe, then China since 2000, to the current position where manufacturing has taken a serious decline as a percentage of GDP. The extent of damage cannot be overstated. The world’s preeminent economic superpower relies completely on its number one adversary for critical minerals, robotics and medical equipment and pharmaceuticals to sustain and grow its industrial base. It is not an overstatement to say that much of the US industry would collapse if China, Japan and Germany colluded to reduce US influence in global affairs. The US does maintain some advantages (it is the largest consumer market) but overall remains at the mercy of other countries.

There are several ramifications for investors of this change in US policy. Firstly we need to understand how investment impacts the economy and how it affect company profits. Broadly, increasing the investment cycle means lower returns since the investment phase eats up excess capital which has previously been returned to shareholders. For example, iPhone manufacturing to America or other friendly countries is more expensive than investing in expansion in China.

Companies that build assets deliver lower returns. These assets are being accumulated by reshoring investment.

Investment is also a driver of mean reversion for both individual companies and whole markets.

For investors it is important to understand how a company will generate profits and how they will be distributed. Demographics means less labour and some of the current high profit margins will be eroded by higher wages even with increased automation (AI will prove disappointing in generating large productivity gains). Profits are distributed between the business owner (capital) and workers (labour). Wages will grow at the expense of profits which means lower returns for capital and shareholders.

A huge investment boom and reshoring requires lots of capital. Imagine a company deciding to build a rare earth processing plant which the US is now undertaking. The bulk of the capital is used to build new facilities and expenses will be high for an extended period. Most funds will need to be borrowed, which, for a period, will require repayment without generating any profits given the considerable lag time between building a factory and generating future profits from that investment. Think of the reduction in Apple’s cash holding from its need to move from China to India and the US. Now multiple that by 500 and you can see an investment boom is great for jobs and economic growth but not for shareholders.

Ignoring valuations, we use the rare earths sectors to demonstrate why we think the US markets will struggle to produce anywhere near the returns that it has delivered over the past 16 years.

RARE EARTH INVESTMENT

MACRO SITUATION

Looking at the rare earth sector, the US has no domestic supply chain and rebuilding one, which it has now started, will take at least a decade. It maybe a stretch, but not much, to argue the US is somewhat akin to an emerging market. Like an emerging market, it needs enormous amounts of physical and human capital to reestablish manufacturing to a point where it can once again be self-sufficient. This will not happen overnight.

MICRO

There will be huge amounts of capital expenditure, depreciation and research and development in the rare earths sector and also the technology sector as the race for AI sees computer chips become obsolete in a short space of time (around 3 years). The United States will need a considerable increase in the supply of labour and with a specific range of skills that contributes to the rebuild of the manufacturing sector including the rare earth sector where there is currently almost no knowledge as it all resides in China.

PROFIT MARGINS

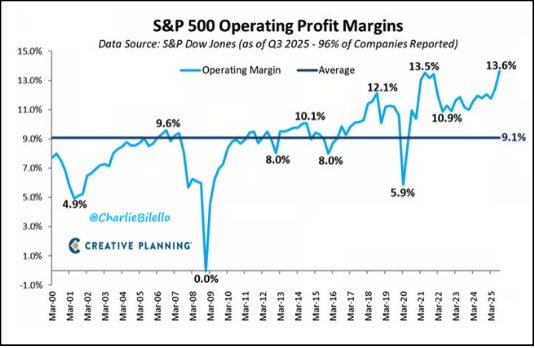

We also expect record corporate profit margins to revert leaving more dollars in the pockets of workers as demographics, falling births rates and reductions in immigration all take effect.

US corporate profits are high because there has been little investment by US firms as manufacturing moved overseas to cheaper locations. The decline of unionisation of the workforce forced workers to compete with countries like China with lower wages. In contrast to this, Japanese firms are not very profitable because of their high investment rates which is why Japanese (Chinese and German) companies can appear cheap from a valuation perspective but investment and asset growth have been elevated resulting in poor corporate profitability

Note Warren Buffett doesn’t like companies that gather assets, spend a lot on research and development, and have high levels of depreciation. The reason why is simple - companies or industries with these characteristics don’t throw off a lot of cash. Shareholders suffer because these companies or industries are required to spend a considerable part of the profits staying competitive. This is especially applicable to technology sectors like those seeking to generate profits from the AI boom. For Buffett, Coke will always be a better investment return than OpenAI because Coke throws of cash thanks to a low depreciation rate, reduced capital expenditure and research and development costs.

SUMMARY

In summary, we see lower returns for the US market and we have been focusing on those sectors, countries, styles and commodities that are currently cheap and offer longer term higher returns. But before increasing the allocation to these asset classes, even though they are cheap, we believe waiting for the US market to offer higher yields or rebalancing your current portfolio is a prudent approach.

Responses