Mastering the Market Cycle: How to Recognise Where We Are Right Now

Jul 04, 2026

Howard Marks says the market cycle is one of the most powerful forces in investing. With the US CAPE ratio sitting around 42, understanding it has rarely mattered more.

On this week's podcast we did something a little different. Instead of the usual run through markets, we sat down with one of the most useful investing books ever written, Howard Marks' Mastering the Market Cycle, and pulled out the ideas that matter most for investors right now.

Here's the thing about market cycles: the charts are blindingly obvious in hindsight. A hundred years of data will teach you the pattern in an afternoon. What the data can't teach you is emotional maturity, and that, not intelligence, is what separates investors who compound wealth from investors who buy the top and sell the bottom.

This post covers the four ideas from the episode that every investor should internalise: why the market is really just people, how the price you pay sets your odds, the three stages of every bull and bear market, and why you don't need to pick the bottom.

Prefer to listen? The full Mastering the Market Cycle special is out now on the Total Money Management podcast. Free subscribers to the Signals & Noise weekly newsletter get the episode and white paper. Signals & Noise Premium members get the complete chapter-by-chapter notes and our current cycle positioning.

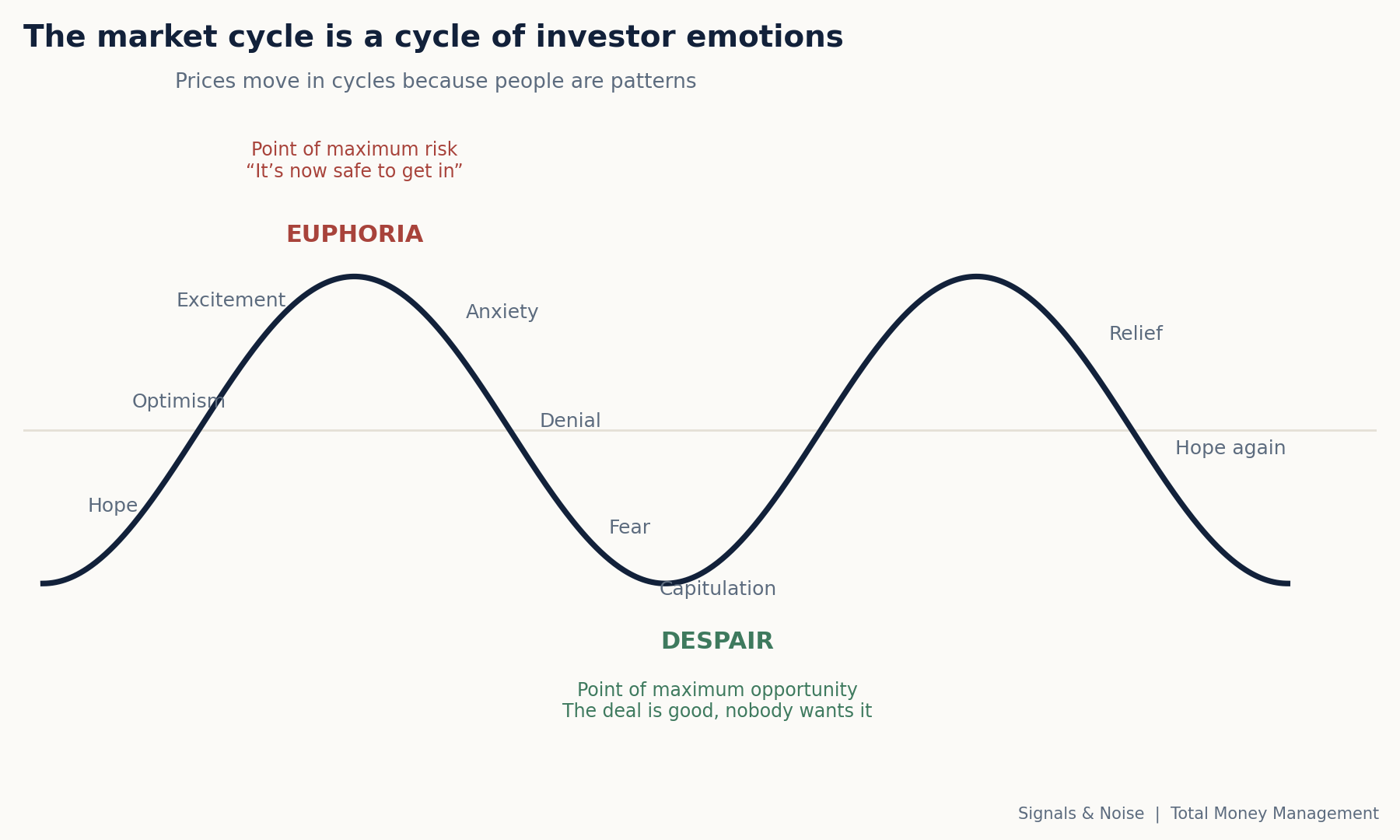

The market cycle is driven by people, not spreadsheets

When people say "the market", they picture something cold and mechanical. A ticker. An index. But strip it back and the market is just a group of people buying and selling to each other. People with emotions, career risk, mortgages, and a deep fear of missing out.

That reframe matters. An objectified "market" doesn't resonate emotionally, but a crowd of anxious, greedy, hopeful humans does. Once you see the market as people, cycles stop being mysterious. People are patterns. They swing between optimism and pessimism, between pricing assets too high and pricing them too low, and they always will.

What about the argument that algorithms now run Wall Street? It's true that machines execute most of the volume. But humans built the machines, humans wrote the inputs, and humans pull the plug when things get scary. The algo is only as unemotional as the person funding it.

Warren Buffett's point stands: if you can't manage your emotions, you can't manage your money. And in our experience, nine out of ten people believe they're the exception. The self-awareness to admit "I might be the emotional one" almost never arrives before the first real loss. Everyone is a genius when the market is going up. Nobody rings their adviser during a rally. The phone only rings on the way down.

The only way to learn is to lose (a little). You don't build emotional resilience by reading about drawdowns, you build it by living through them. That's why we tell new investors to start with a small amount of money and earn a "corporate memory" of bad days before committing serious capital. Feel what it's like to lose money without actually losing much money. It's the same as learning guitar: you don't buy the expensive instrument and book a gig in week one.

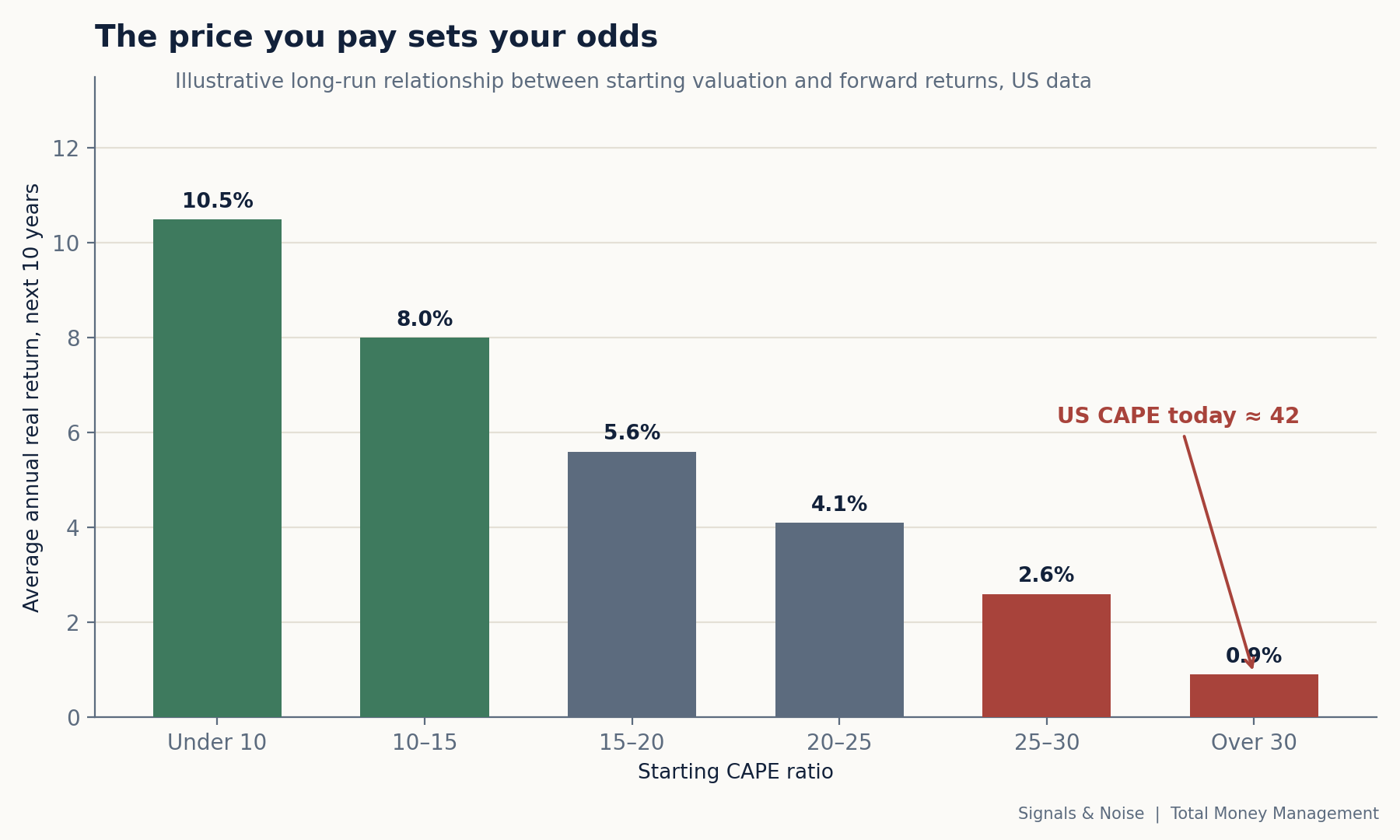

The price you pay sets your odds: the CAPE ratio at 42

Marks' central insight is that superior investing doesn't come from buying high-quality assets. It comes from buying well, when the price is low, the potential return is substantial, and the risk is limited. It's not what you buy that determines your results, it's what you pay.

Our favourite tool for measuring that is the CAPE ratio (cyclically adjusted price-to-earnings). Over the last century it has ranged from single digits at generational lows to the low forties at generational peaks. Today the US market sits at roughly 42.

This isn't a prediction that the market crashes tomorrow. It's a statement about probabilities. When the CAPE is at 8 or 12, the odds of strong ten-year returns are heavily in your favour, and we'd be telling people to pile in. At 42, the odds of the next decade repeating the last one are very low. Unemotional investing means looking at those numbers and asking one question: what are my chances?

The same logic applies globally. Cheap markets like Turkey (CAPE around 10) or Colombia (around 6) can absolutely get cheaper if the US catches a cold, and when the US sneezes, everyone does. But the research is consistent: markets that are cheap on a CAPE basis may fall further in the short run, yet still deliver better long-run returns than expensive ones. You might be buying a dollar for forty cents and watching it trade to ten cents first. That's uncomfortable, not wrong.

We track global CAPE ratios, earnings yields and trend signals every week in Signals & Noise. The free weekly market newsletter gives you the headline read. Signals & Noise Premium members get the full macro valuation data and CAPE analysis, our ETF and portfolio positioning, and the reasoning behind it. Sign up to Signals & Noise free and take the investor quiz here.

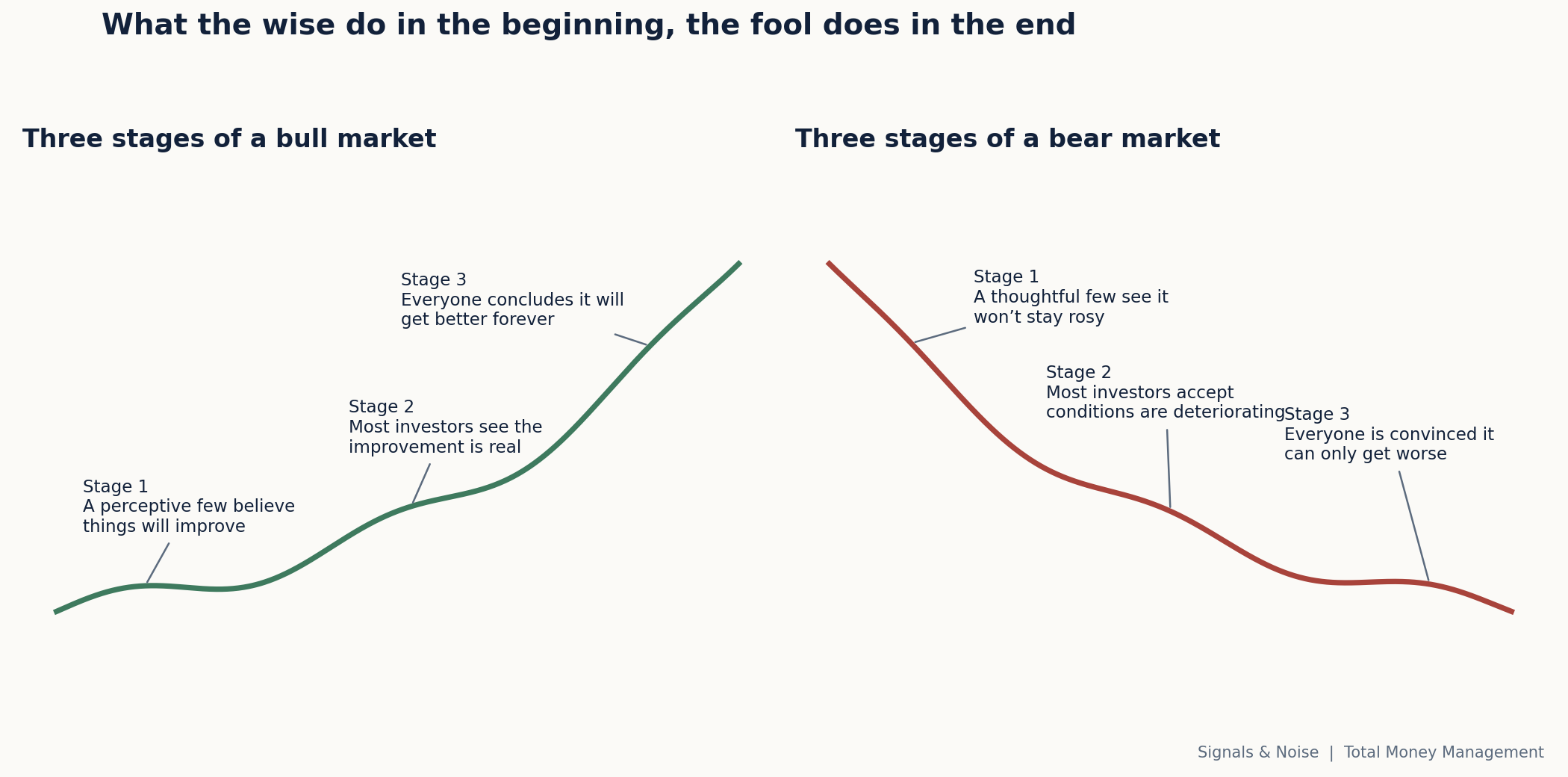

The three stages of every bull and bear market

Marks describes each bull market in three stages. Early on, only a perceptive few believe conditions will improve. In the middle, the majority accepts the recovery is real. At the end, everyone concludes prices will rise forever. His famous line sums it up: "what the wise man does in the beginning, the fool does in the end."

The cruel mechanics of stage three: the most risk-averse investors are typically the last ones in, precisely because they waited until it finally "felt safe". Everyone around them is making money, the headlines are euphoric, and the social proof is overwhelming. That feeling of safety is the signal of maximum danger. It's the zebra wandering down to the waterhole just as the crocodile surfaces.

Where are we now? Our read from the episode: the US market looks like textbook stage three of a bull market, while several emerging markets have spent recent years grinding through stage two or three of a bear market. That divergence is exactly where contrarian opportunity tends to live, and exactly where it feels worst to act.

Notice too that none of this is analytical. Nobody in the suburbs is reading the producer price index and rationally concluding it's time to buy. People don't think the market will get better. They feel it will, because everyone at the barbecue is talking about stocks. Investor rationality is the exception, not the rule.

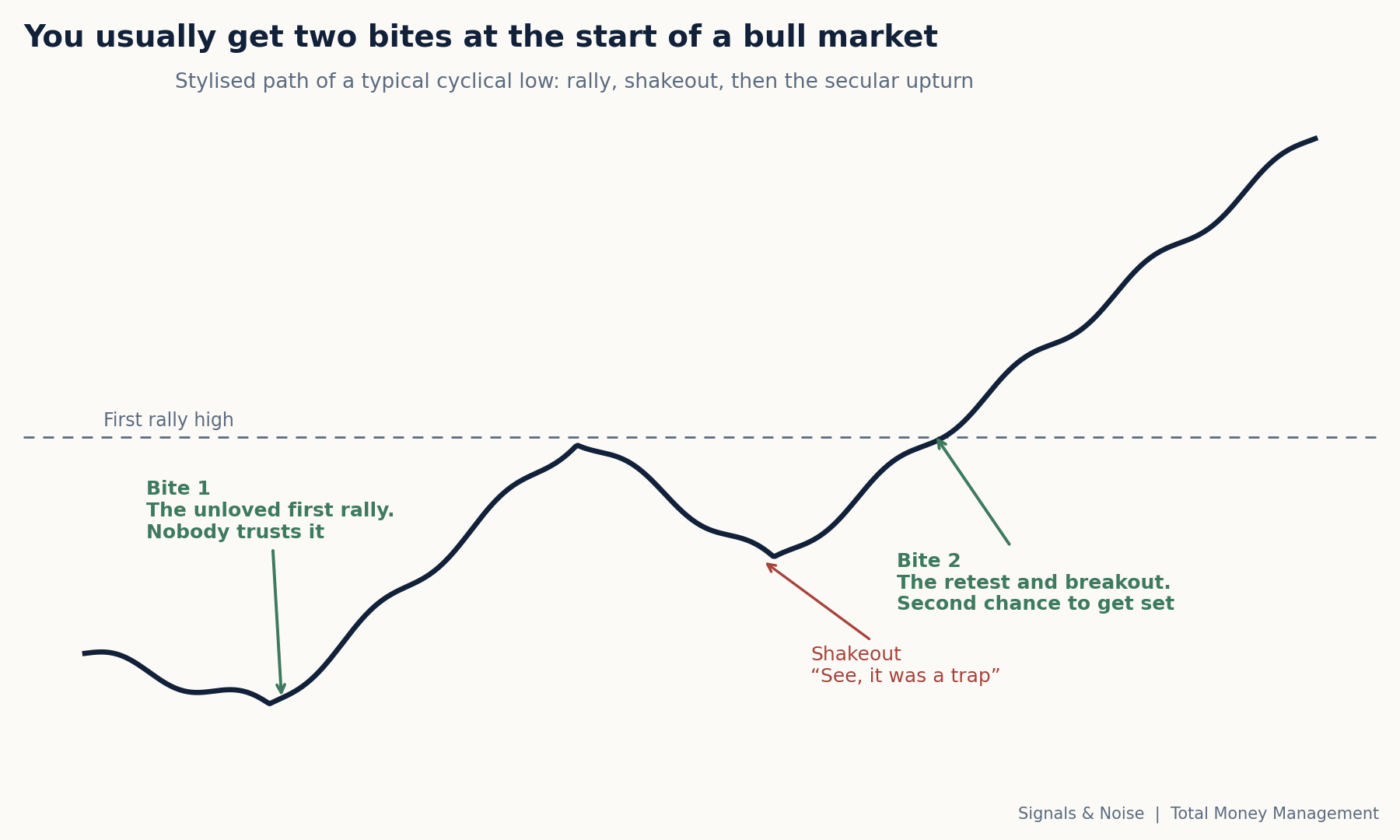

You don't need to pick the bottom (and you'll usually get two bites)

The most paralysing myth in investing is that you have to nail the turn. You don't. The 2009 bottom arrived on March 9. Buying heavily in April, a month "late", still produced spectacular results. In fact, buying at almost any point in the following twelve months worked out fine, because the starting valuation was cheap and the earnings yield was high.

History offers another comfort: new bull markets usually give you two chances to get set. The first rally off the low is distrusted, sentiment is still awful, and a scare eventually knocks it back down. Then the market stabilises, breaks the previous high, and the real secular upturn begins.

This is why we lean on simple, unemotional rules rather than prediction:

Valuation plus trend. Use CAPE to know whether the deal is good, and a simple tool like the 200-day moving average to know whether momentum is with you. This is the exact framework we teach in Well 2 of the Three Wells program: assessing global market valuations with CAPE and rotating between ETFs using momentum signals. An expensive market above trend can keep running. An expensive market breaking below trend is a very different animal to a cheap one doing the same thing.

Rebalancing and asset allocation. Decide your split, review on a fixed schedule (say quarterly), and let the rules move you toward cheap assets and away from expensive ones. You never go all-in, you always hold some cash, and falling prices become an opportunity to buy more rather than a reason to panic.

Position for the fat pitch. Skilled investors think like professional gamblers: zero emotion, total respect for probabilities, and above all, survival. Rule number one is staying in the game. You can be wrong seven times out of eight if, when the genuinely great opportunity arrives, you have the cash and the nerve to swing hard.

This is exactly what Signals & Noise Premium is built for: the weekly signals that tell you when the odds shift, and the framework to act on them without the emotion. Free members get the Signals & Noise newsletter every Saturday. Premium members get weekly ETF and portfolio positioning, macro valuation data, monthly deep-dive research reports and live group coaching calls, for $9.99 a week. Upgrade to Signals & Noise Premium here.

The bottom line

Cycles will never stop, because the human tendency to run to excess will never stop. Every excess eventually corrects, and every correction eventually plants the seeds of the next boom. Investors who understand that rhythm, and who can keep their emotions parked while everyone around them is euphoric or despairing, will keep finding opportunities to profit from it.

Right now, the numbers say the US market is priced for perfection while much of the rest of the world is priced for pessimism. You can't control which way it breaks or when. You can control what you pay, how you allocate, and whether you follow your rules or your feelings. Success in markets teaches people that making money is easy and risk doesn't matter. That lesson is always unlearned the hard way.

Want the full breakdown? We've condensed all seventeen chapters of Mastering the Market Cycle into a Signals & Noise white paper. It's free for newsletter subscribers, and Premium members also get our chapter-by-chapter notes plus where we're positioned right now. Sign up free to get the Mastering the Market Cycle white paper.

Frequently asked questions

What is the market cycle in investing? The market cycle is the recurring swing of asset prices from undervalued to overvalued and back again. It's driven less by economics and more by investor psychology: optimism pushes prices above fair value, fear pushes them below it, and the pattern repeats because human behaviour repeats.

How do I know where we are in the market cycle? You can't pick exact tops or bottoms, but you can assess the odds. Combine a valuation measure like the CAPE ratio with a simple trend measure like the 200-day moving average, then observe behaviour around you. Extreme valuations plus universal confidence usually means late cycle. We publish our weekly read in the Signals & Noise newsletter.

What does a CAPE ratio of 42 mean? It means US shares cost roughly 42 times their inflation-adjusted ten-year average earnings. Historically, starting valuations this high have been followed by very low, sometimes negative, real returns over the following decade.

Should I wait for the bottom before investing? No. Nobody picks the exact bottom and you don't need to. Buying anywhere near a cyclical low, when valuations are cheap and yields are high, has historically produced strong long-run results. Rebalancing rules and staged entries remove the need for perfect timing.

General advice warning: This article contains general information only and does not take into account your objectives, financial situation or needs. It is not personal financial advice. Before acting on any information, consider its appropriateness to your circumstances and seek advice from a licensed financial adviser. Past performance is not a reliable indicator of future performance. Total Money Management, AFSL 568642.

Enjoying our Blogs?

Our Investing Essentials subscription might be worth looking into, get more specific detail below if you're interested in upskilling.

Stay connected to our blog

Join our mailing list to receive the latest news and updates from our team including blogs, live events, podcast releases and stocks to watch.

Your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.